KRATOS DEFENSE & SECURITY SOLUTIONS (KTOS)·Q4 2025 Earnings Summary

Kratos Beats on All Metrics as Valkyrie Wins Fuel Record Backlog

February 23, 2026 · by Fintool AI Agent

Kratos Defense & Security Solutions (NASDAQ: KTOS) delivered a triple beat in Q4 2025, with revenue up 22% year-over-year to $345M and adjusted EPS surging 38% to $0.18. The defense technology company reported record backlog of $1.57B and a record opportunity pipeline of $13.7B following its Valkyrie CCA program win with Northrop Grumman.

CEO Eric DeMarco struck a bullish tone: "Generating a 1.3 to 1 book-to-bill ratio on top of 20% organic growth, while also maintaining a record-high backlog and record-high opportunity pipeline, we believe is representative of the increasing demand for Kratos' affordable military-grade hardware and software, and that our growth trajectory is accelerating."

Did Kratos Beat Earnings?

Kratos beat consensus estimates across all three key metrics, continuing its streak of consistent outperformance.

The revenue beat was driven by strong execution across both segments, with organic growth of 20.0% versus management's prior estimate of 14-15%. The largest contributors to the overachievement were Space and Satellite, Turbine Technologies, C5ISR, and Microwave Products businesses.

What Drove the Outperformance?

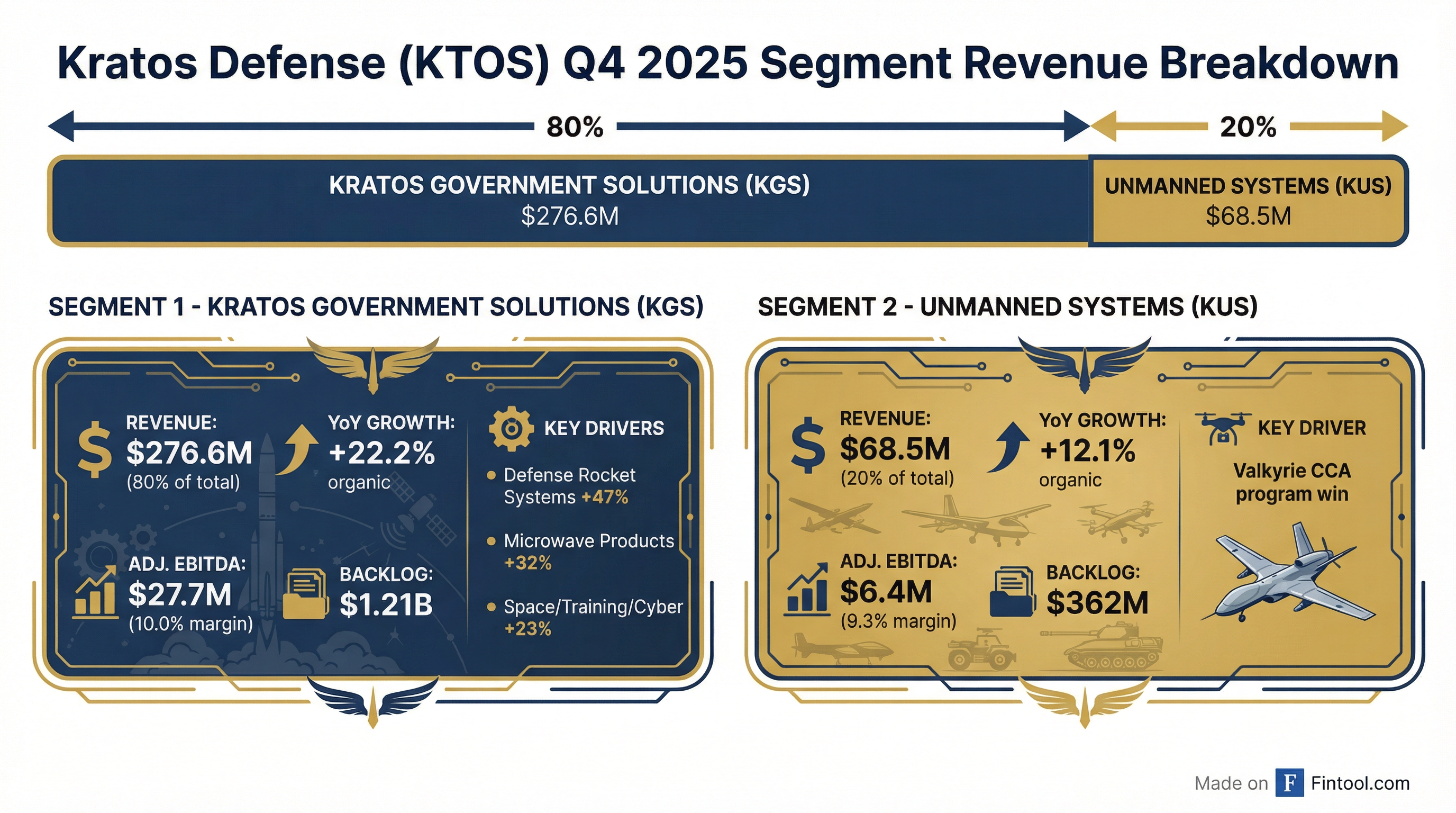

Segment Performance

Kratos Government Solutions (KGS) — The larger segment delivered exceptional results with 22.2% organic revenue growth.

Unmanned Systems (KUS) — The tactical drone segment grew 12.1% organically, driven primarily by Valkyrie-related activity.

What Did Management Guide?

Kratos provided FY 2026 guidance reflecting 13-19% organic growth, with Q1 expected to be the low point.

Q1 2026 Guidance: Revenue of $335-345M and Adjusted EBITDA of $25-30M. Management noted: "Q1 will be the lowest, including as we come off another CRA and also this time a government shutdown, both of which are now resolved, and we will ramp throughout the year."

The guidance does not include the pending Orbit Technologies acquisition, which is expected to close by end of Q1.

Hypersonic Franchise: The Growth Engine

The hypersonic business emerged as the primary growth driver, with DeMarco providing detailed revenue trajectory:

Key developments:

- 120 Zeus and Oriole solid rocket motors now on order, with deliveries beginning Q3 2026

- Selected by Pentagon to develop highly maneuverable Mach 5+ hypersonic missiles under the Joint Hypersonics Transition Office

- Expecting an additional ~$1B+ hypersonic opportunity by year-end, believed to be sole-sourced to Kratos

- Maryland hypersonic facility operational; Indiana integration facility and Birmingham expansion coming online

When asked about the biggest growth driver, DeMarco was emphatic: "The hypersonic franchise... this will drive our growth trajectory and our profitability for the foreseeable future."

Space and Satellite: Record Backlog, Major Win

Kratos' space and satellite business, the company's largest, achieved record backlog of $600M with a 1.2x book-to-bill ratio.

Key developments:

- Completed factory acceptance testing between Kratos' Epic C2 software and Airbus OneSat next-gen software-defined satellite platform

- Informed of selection for an initial ~$500M program award

- Global Space Domain Awareness system with ~190 worldwide sensors across 20+ sites

DeMarco highlighted the strategic positioning: "Kratos' OpenSpace satellite software is the only software-defined networking solution designed so that virtually every piece of the satellite ground station can now be turned into software... This is one of the software jewels of our company."

Valkyrie CCA: What's the Unit Economics?

Northrop Grumman won the MUX TACAIR CCA program with Kratos Valkyrie as the aircraft. DeMarco provided clarity on the revenue model:

Per-Aircraft Revenue to Kratos: ~$10M (not 50/50 split of program value)

"Don't look at it that way... Look at $10 million per aircraft for Kratos. Might be a little less, might be a little more, depending on the configuration."

Production Ramp Plan:

- Current rate: ~8 aircraft annually

- Target rate: ~40 aircraft annually by end of 2028

- CapEx for production ramp: $25-28M in FY 2026

DeMarco emphasized Kratos' competitive positioning: "We're kind of, sort of turning into the merchant supplier of tactical jet drones, because we're the only guy that has anything flying right now."

Turbine Technologies: Engine Production Ramping

The jet engine business is approaching an inflection point:

- GE Aerospace partnership: Received Air Force award to design engine for expendable Combat Collaborative Aircraft (CCA)

- LRIP starting H2 2026: Small engine low-rate initial production for certain missile programs

- 15,000 engine RFQ: Responding to customer quote for a system designed around Kratos Spartan jet engine

- New 40,000 engine/year capacity facility in Michigan now operational

Per-engine economics: $40,000-50,000 per engine

DeMarco outlined the trajectory: "Second half of 2028, we could see a step function... delivering hundreds of engines, and we're getting ready to build thousands of engines to deliver in 2029."

Microwave Electronics: Under-the-Radar Growth

The microwave business grew 17% organically in FY 2025 and DeMarco identified it as a key future growth driver.

Major Programs:

- Iron Dome

- Arrow

- Barak

- David's Sling

- SPYDER

- Plus 2 classified U.S. programs

Revenue Mix: ~50-60% tied to missile and air defense programs, ~20% satellite communications, remainder in comms systems

"Virtually every system globally, whether it be a missile, a radar, an air defense, a drone, needs microwave electronics. We are all over it."

Prometheus JV: Long-Term Growth Vehicle

The solid rocket motor and energetics joint venture with Rafael broke ground last week. DeMarco provided the financial trajectory:

Margins: ~20% at full rate production

Kratos Economics: 49.9% ownership; equity method accounting (one-line income/loss, no revenue consolidation)

Acquisitions: Nomad and Orbit

Nomad Global Communication Solutions — Closed mid-February 2026

- LTM Revenue: ~$75M

- Focus: Mobile command, control, and communication systems for unmanned systems, counter-UAS, and homeland security

- Strategic rationale: "If you're static, you're dead. There are a significant number of programs coming for mobile systems."

Orbit Technologies — Expected to close by end of Q1

- Israeli-based satellite communications company

- Not yet included in guidance

Q&A Highlights

On Anduril's $60B valuation and defense tech multiples:

"I believe that Kratos is the most valuable defense company in the industry, private or public... We have a balanced approach. We're gonna organically grow the company, invest significant amounts to rebuild the industrial base, but always be mindful of generating an adequate return on investment for investors."

On why Northrop is prime on Valkyrie (not Kratos):

"Our probability of win is much higher with Northrop as the prime than if Kratos was the prime. Additionally, it reduces risk to Kratos on the integration of those very exquisite mission systems. We are getting a full stop profit margin on the aircraft."

On contract recompete risk:

"There is nothing of significance rolling off. We have zero recompetes of any size for the foreseeable future."

On prime contractor relationships:

"We really don't compete with the traditional primes. We partner with them... What the primes are doing now and leaning forward, this is going to be an accelerator for Kratos."

On budget sensitivity:

"We are in great shape to achieve, if not exceed, our forecast for '26 and '27, with it potentially accelerating in '28 and '29... under current funding, normal growth. If budgets go from $1 trillion to $1.5 trillion, I believe that's going to be very good for us."

Three Catalysts to Watch (Per CEO)

When asked about the most important near-term catalysts, DeMarco identified three:

- ~$1B+ Hypersonic Sole-Source Award — Expected by year-end

- Another Tactical Drone CCA Program Announcement — Customer-dependent timing

- Jet Engine Production Contract — Could be announced by a prime

Forward Catalysts (Full List)

- Valkyrie production ramp — Scaling to 40 units annually by end of 2028

- Hypersonic franchise doubling — From ~$200M to ~$400M in FY26

- ~$1B hypersonic opportunity — Expected sole-source award by year-end

- Space business $500M program — Recently awarded

- Jet engine LRIP — Starting H2 2026

- Orbit Technologies acquisition — Pending close

- Mighty Hornet Taiwan — Production decision possible Q4 2026

- Prometheus production — Beginning H2 2027

Risks and Concerns

- Government shutdown impact — Q1 2026 will be soft due to delayed contract awards from Q4 2025 shutdown

- Fixed-price contract pressure — Material and subcontractor cost increases on multi-year contracts continue to weigh on margins

- Heavy investment phase — $135-145M capex plus $50M Prometheus JV funding in FY26

- DSO expansion — Days Sales Outstanding increased from 111 to 121 days due to government shutdown impacts on payment timing

- Appropriations timing — 2027 federal budget approval timing could impact H2 2027 revenue recognition

Full Year 2025 Results

Data sourced from Kratos Defense Q4 2025 earnings call transcript and S&P Global. Stock prices as of market close February 23, 2026.